Stock Market

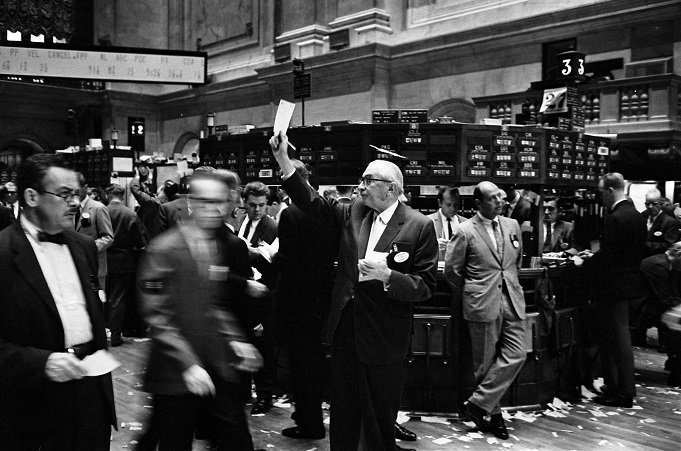

Wall Street October 1929

Stock Market: Claud Cockburn, writing for the "Times of London" from New-York, described the irrational exuberance that gripped the nation just prior to the Great Depression. As Europe wallowed in post-war malaise, America seemed to have discovered a new economy, the secret of uninterrupted growth and prosperity, the fount of transforming technology: "The atmosphere of the great boom was savagely exciting, but there were times when a person with European background felt alarmingly lonely.

He would have liked to believe, as these people believed, in the eternal upswing of the big bull market or else to meet just one person with whom he might discuss some general doubts without being regarded as an imbecile or a person of deliberately evil intent - some kind of anarchist, perhaps." The greatest analysts with the most impeccable credentials and track records failed to predict the forthcoming crash and the unprecedented economic depression that followed it. Irving Fisher, a preeminent economist, who, according to his biographer-son, Irving Norton Fisher, lost the equivalent of $140 million in today's money in the crash, made a series of soothing predictions.

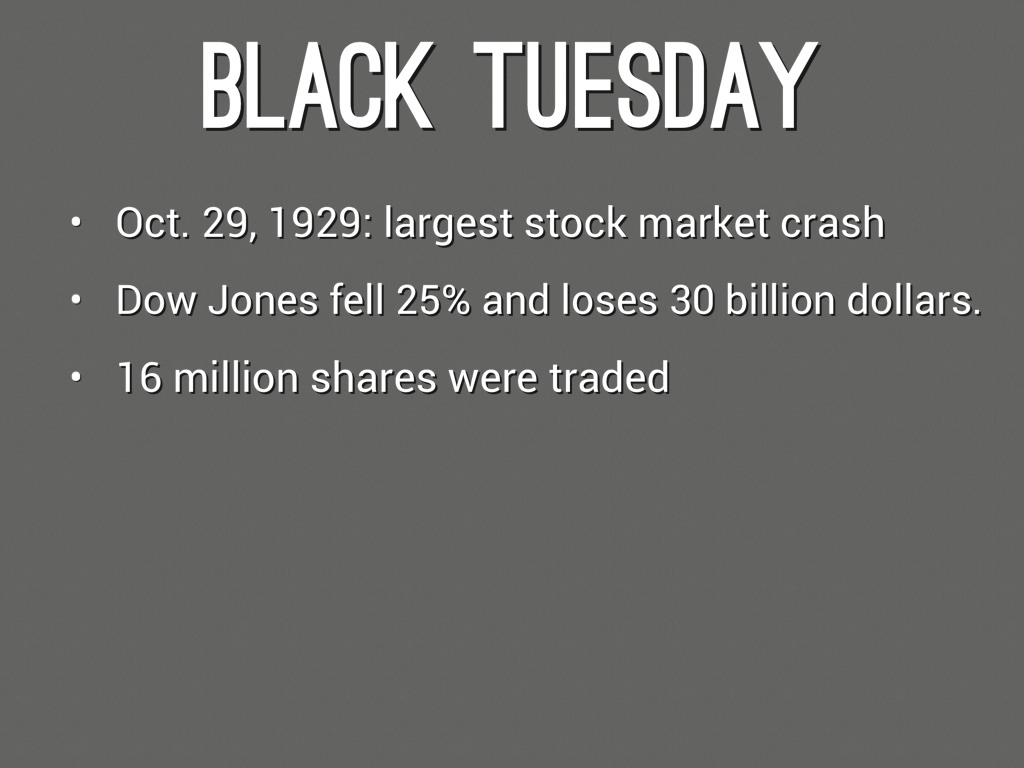

On October 22 he uttered these avuncular statements: "Quotations have not caught up with real values as yet ... (There is) no cause for a slump ... The market has not been inflated but merely readjusted..." Even as the market convulsed on Black Thursday, October 24, 1929 and on Black Tuesday, October 29 - the New York Times wrote: "Rally at close cheers brokers, bankers optimistic". In an editorial on October 26, it blasted rabid speculators and compliant analysts: "We shall hear considerably less in the future of those newly invented conceptions of finance which revised the principles of political economy with a view solely to fitting the stock market's vagaries.''

But it ended thus: "(The Federal Reserve has) insured the soundness of the business situation when the speculative markets went on the rocks.'' Compare this to Alan Greenspan Congressional testimony this summer: "While bubbles that burst are scarcely benign, the consequences need not be catastrophic for the economy ... (The Depression was brought on by) ensuing failures of policy." Investors, their equity leveraged with bank and broker loans, crowded into stocks of exciting "new technologies", such as the radio and mass electrification.

FrizeMedia Ghana SEO SEM Digital Marketing Proposal

The Best And Top Digital Marketing And SEO Services In Ghana

The bull market - especially in issues of public utilities - was fueled by "mergers, new groupings, combinations and good earnings" and by corporate purchasing for "employee stock funds". Cautionary voices - such as Paul Warburg, the influential banker, Roger Babson, the "Prophet of Loss" and Alexander Noyes, the eternal Cassandra from the New York Times - were derided. The number of brokerage accounts doubled between March 1927 and March 1929. When the market corrected by 8 percent between March 18-27 - following a Fed induced credit crunch and a series of mysterious closed-door sessions of the Fed's board - bankers rushed in.

The New York Times reported: "Responsible bankers agree that stocks should now be supported, having reached a level that makes them attractive.'' By August, the market was up 35 percent on its March lows. But it reached a peak on September 3 and it was downhill since then. On October 19, five days before "Black Thursday", Business Week published this sanguine prognosis: "Now, of course, the crucial weaknesses of such periods - price inflation, heavy inventories, over-extension of commercial credit - are totally absent.

The security market seems to be suffering only an attack of stock indigestion... There is additional reassurance in the fact that, should business show any further signs of fatigue, the banking system is in a good position now to administer any needed credit tonic from its excellent Reserve supply." The crash unfolded gradually. Black Thursday actually ended with an inspiring rally. Friday and Saturday - trading ceased only on Sundays - witnessed an upswing followed by mild profit taking. The market dropped 12.8 percent on Monday, with Winston Churchill watching from the visitors' gallery - incurring a loss of $10-14 billion.

The Wall Street Journal warned naive investors: "Many are looking for technical corrective reactions from time to time, but do not expect these to disturb the upward trend for any prolonged period." The market plummeted another 11.7 percent the next day - though trading ended with an impressive rally from the lows. October 31 was a good day with a "vigorous, buoyant rally from bell to bell". Even Rockefeller joined the myriad buyers.

Shares soared. It seemed that the worst was over. The New York Times was optimistic: "It is thought that stocks will become stabilized at their actual worth levels, some higher and some lower than the present ones, and that the selling prices will be guided in the immediate future by the worth of each particular security, based on its dividend record, earnings ability and prospects. Little is heard in Wall Street these days about 'putting stocks up." Little is heard in Wall Street these days about 'putting stocks up."

But it was not long before irate customers began blaming their stupendous losses on advice they received from their brokers. Alec Wilder, a songwriter in New York in 1929, interviewed by Stud Terkel in "Hard Times" four decades later, described this typical exchange with his money manager: "I knew something was terribly wrong because I heard bellboys, everybody, talking about the stock market. About six weeks before the Wall Street Crash, I persuaded my mother in Rochester to let me talk to our family adviser.

I wanted to sell stock which had been left me by my father. He got very sentimental: 'Oh your father wouldn't have liked you to do that.' He was so persuasive, I said O.K. I could have sold it for $160,000. Four years later, I sold it for $4,000." Exhausted and numb from days of hectic trading and back office operations, the brokerage houses pressured the stock exchange to declare a two day trading holiday.

Exchanges around North America followed suit. At first, the Fed refused to reduce the discount rate. "(There) was no change in financial conditions which the board thought called for its action." - though it did inject liquidity into the money market by purchasing government bonds. Then, it partially succumbed and reduced the New York discount rate, which, curiously, was 1 percent above the other Fed districts - by 1 percent. This was too little and too late.

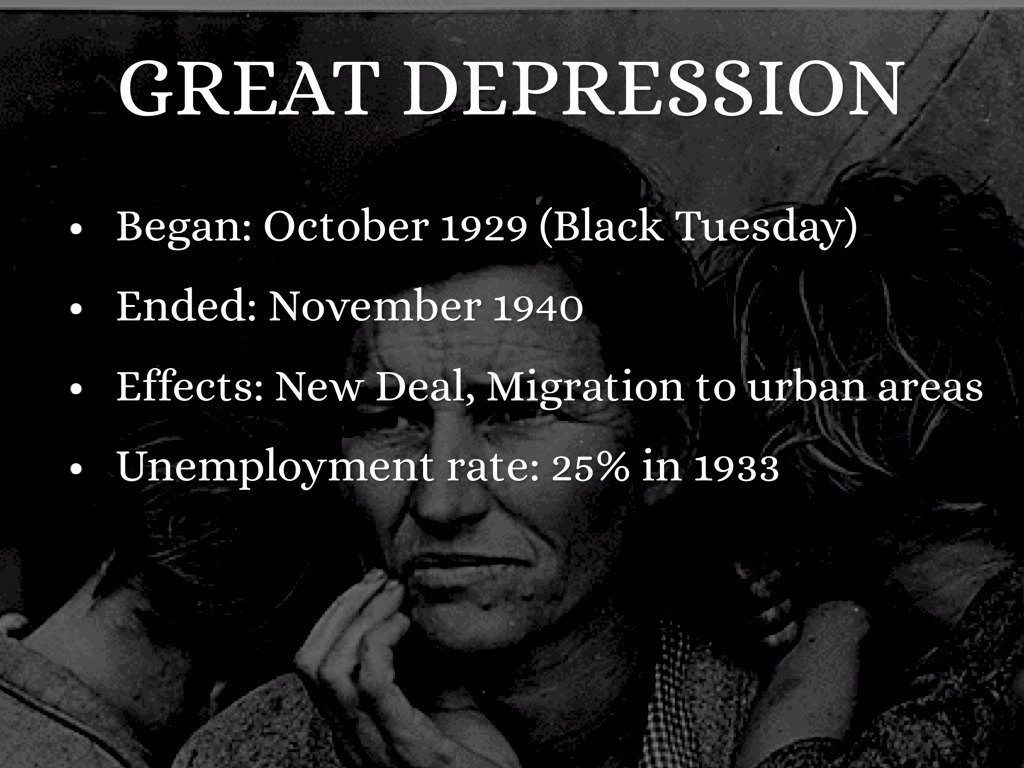

The market never recovered after November 1. Despite further reductions in the discount rate to 4 percent, it shed a whopping 89 percent in nominal terms when it hit bottom three years later. Everyone was duped. The rich were impoverished overnight. Small time margin traders - the forerunners of today's day traders - lost their shirts and much else besides.

The New York Times: "Yesterday's market crash was one which largely affected rich men, institutions, investment trusts and others who participate in the market on a broad and intelligent scale.

It was not the margin traders who were caught in the rush to sell, but the rich men of the country who are able to swing blocks of 5,000, 10,000, up to 100,000 shares of high-priced stocks. They went overboard with no more consideration than the little trader who was swept out on the first day of the market's upheaval, whose prices, even at their lowest of last Thursday, now look high by comparison. To most of those who have been in the market it is all the more awe-inspiring because their financial history is limited to bull markets." Overseas - mainly European - selling was an important factor.

Some conspiracy theorists, such as Webster Tarpley in his "British Financial Warfare", supported by contemporary reporting by the likes of "The Economist", went as far as writing: "When this Wall Street Bubble had reached gargantuan proportions in the autumn of 1929, (Lord) Montagu Norman (governor of the Bank of England 1920-1944) sharply (upped) the British bank rate, repatriating British hot money, and pulling the rug out from under the Wall Street speculators, thus deliberately and consciously imploding the US markets.

This caused a violent depression in the United States and some other countries, with the collapse of financial markets and the contraction of production and employment. In 1929, Norman engineered a collapse by puncturing the bubble." The crash was, in large part, a reaction to a sharp reversal, starting in 1928, of the reflationary, "cheap money", policies of the Fed intended, as Adolph Miller of the Fed's Board of Governors told a Senate committee, "to bring down money rates, the call rate among them, because of the international importance the call rate had come to acquire.

The purpose was to start an outflow of gold - to reverse the previous inflow of gold into this country (back to Britain)." But the Fed had already lost control of the speculative rush. The crash of 1929 was not without its Enrons and World.com's. Clarence Hatry and his associates admitted to forging the accounts of their investment group to show a fake net worth of $24 million British pounds - rather than the true picture of 19 billion in liabilities.

This led to forced liquidation of Wall Street positions by harried British financiers. The collapse of Middle West Utilities, run by the energy tycoon, Samuel Insull, exposed a web of offshore holding companies whose only purpose was to hide losses and disguise leverage. The former president of NYSE, Richard Whitney was arrested for larceny. Analysts and commentators thought of the stock exchange as decoupled from the real economy.

Only one tenth of the population were investors - compared to 40 percent today. "The World" wrote, with more than a bit of Schadenfreude: "The country has not suffered a catastrophe ... The American people ... has been gambling largely with the surplus of its astonishing prosperity." "The Daily News" concurred: "The sagging of the stocks has not destroyed a single factory, wiped out a single farm or city lot or real estate development, decreased the productive powers of a single workman or machine in the United States."

Options Trading - Why Trade Options?

In Louisville, the "Herald Post" commented sagely: "While Wall Street was getting rid of its weak holder to their own most drastic punishment, grain was stronger. That will go to the credit side of the national prosperity and help replace that buying power which some fear has been gravely impaired." During the Coolidge presidency, according to the Encyclopedia Britannica, "stock dividends rose by 108 percent, corporate profits by 76 percent, and wages by 33 percent. In 1929, 4,455,100 passenger cars were sold by American factories, one for every 27 members of the population, a record that was not broken until 1950. Productivity was the key to America's economic growth.

Because of improvements in technology, overall labour costs declined by nearly 10 percent, even though the wages of individual workers rose." Jude Waninski adds in his tome "The Way the World Works" that "between 1921 and 1929, GNP grew to $103.1 billion from $69.6 billion. And because prices were falling, real output increased even faster." Tax rates were sharply reduced. John Kenneth Galbraith noted these data in his seminal "The Great Crash":

"Between 1925 and 1929, the number of manufacturing establishments increased from 183,900 to 206,700; the value of their output rose from $60.8 billions to $68 billions. The Federal Reserve index of industrial production which had averaged only 67 in 1921 ... had risen to 110 by July 1928, and it reached 126 in June 1929 ... (but the American people) were also displaying an inordinate desire to get rich quickly with a minimum of physical effort." Personal borrowing for consumption peaked in 1928 - though the administration, unlike today, maintained twin fiscal and current account surpluses and the USA was a large net creditor.

Charles Kettering, head of the research division of General Motors described consumeritis thus, just days before the crash: "The key to economic prosperity is the organized creation of dissatisfaction." Inequality skyrocketed. While output per man-hour shot up by 32 percent between 1923 and 1929, wages crept up only 8 percent. In 1929, the top 0.1 percent of the population earned as much as the bottom 42 percent. Business-friendly administrations reduced by 70 percent the exorbitant taxes paid by those with an income of more than $1 million. But in the summer of 1929, businesses reported sharp increases in inventories.

It was the beginning of the end. Were stocks overvalued prior to the crash? Did all stocks collapse indiscriminately? Not so. Even at the height of the panic, investors remained conscious of real values. On November 3, 1929 the shares of American Can, General Electric, Westinghouse and Anaconda Copper were still substantially higher than on March 3, 1928. John Campbell and Robert Shiller, author of "Irrational Exuberance", calculated, in a joint paper titled "Valuation Ratios and the Lon-Run Market Outlook: An Update" posted on Yale University' s Web Site, that share prices divided by a moving average of 10 years worth of earnings reached 28 just prior to the crash. Contrast this with 45 on March 2000.

In an NBER working paper published December 2001 and tellingly titled "The Stock Market Crash of 1929 - Irving Fisher was Right", Ellen McGrattan and Edward Prescott boldly claim: "We find that the stock market in 1929 did not crash because the market was overvalued. In fact, the evidence strongly suggests that stocks were undervalued, even at their 1929 peak." According to their detailed paper, stocks were trading at 19 times after-tax corporate earning at the peak in 1929, a fraction of today's valuations even after the recent correction. A March 1999 "Economic Letter" published by the Federal Reserve Bank of San-Francisco wholeheartedly concurs.

It notes that at the peak, prices stood at 30.5 times the dividend yield, only slightly above the long term average. Contrast this with an article published in June 1990 issue of the "Journal of Economic History" by Robert Barsky and Bradford De Long and titled "Bull and Bear Markets in the Twentieth Century": "Major bull and bear markets were driven by shifts in assessments of fundamentals: investors had little knowledge of crucial factors, in particular the long run dividend growth rate, and their changing expectations of average dividend growth plausibly lie behind the major swings of this century." Jude Waninski attributes the crash to the disintegration of the pro-free-trade coalition in the Senate which later led to the notorious Smoot-Hawley Tariff Act of 1930.

He traces all the important moves in the market between March 1929 and June 1930 to the intricate protectionist danse macabre in Congress. This argument may never be decided. Is a similar crash on the cards? This cannot be ruled out. Are we ready for a recurrence of 1929? About as we were prepared in 1928. Human nature - the prime mover behind market meltdowns - seemed not to have changed that much in these intervening eight decades. Will a stock market crash, should it happen, be followed by another "Great Depression"? It depends which kind of crash.

The short term puncturing of a temporary bubble - e.g., in 1962 and 1987 - is usually divorced from other economic fundamentals. But a major correction to a lasting bull market invariably leads to recession or worse. As the economist Hernan Cortes Douglas reminds us in "The Collapse of Wall Street and the Lessons of History" published by the Friedberg Mercantile Group, this was the sequence in London in 1720 (the infamous "South Sea Bubble"), and in the USA in 1835-40 and 1929-32.

Differences Between Stocks That Are Down And Out

Understanding The Stock Market

Greed And Fear Are Major Factors In The Stock Market

What Does Your Credit Rating Say About You?

InternetBusinessIdeas-Viralmarketing Home Page

Tweet

Follow @Charlesfrize

{kind=link}

{kind=link}

{kind=link}