Stock Market

Wall Street October 1929

Stock Market: From his vantage point in New York, Claud Cockburn of the Times of London chronicled the feverish optimism that defined America just before the Great Depression. As a war-weary Europe stagnated, the U.S. seemed to have discovered a perpetual motion machine for its economy, driven by transformative technology and the promise of endless prosperity. Cockburn conveyed the scene's duality: "The atmosphere of the great boom was savagely exciting, but there were times when a person with European background felt alarmingly lonely."

He wanted to share their faith in the market’s eternal ascent, to believe as they did in its boundless upward surge. Or, failing that, he longed to find even one person with whom he could voice his quiet doubts, without being dismissed as a fool, a cynic, or worse, some sort of anarchist.

Yet even the most respected analysts, those with impeccable credentials and flawless track records, had been blindsided. Not one foresaw the crash or the unprecedented depression that followed. Irving Fisher, a titan of economics, had issued a string of reassuring forecasts, only to watch his fortune vanish. According to his son and biographer, Irving Norton Fisher, the losses he sustained would amount to roughly $140 million in today’s currency.

On October 22, he offered reassuring, almost paternal statements: “Quotations have not yet caught up with real values... There is no cause for a slump... The market has not been inflated but merely readjusted.”

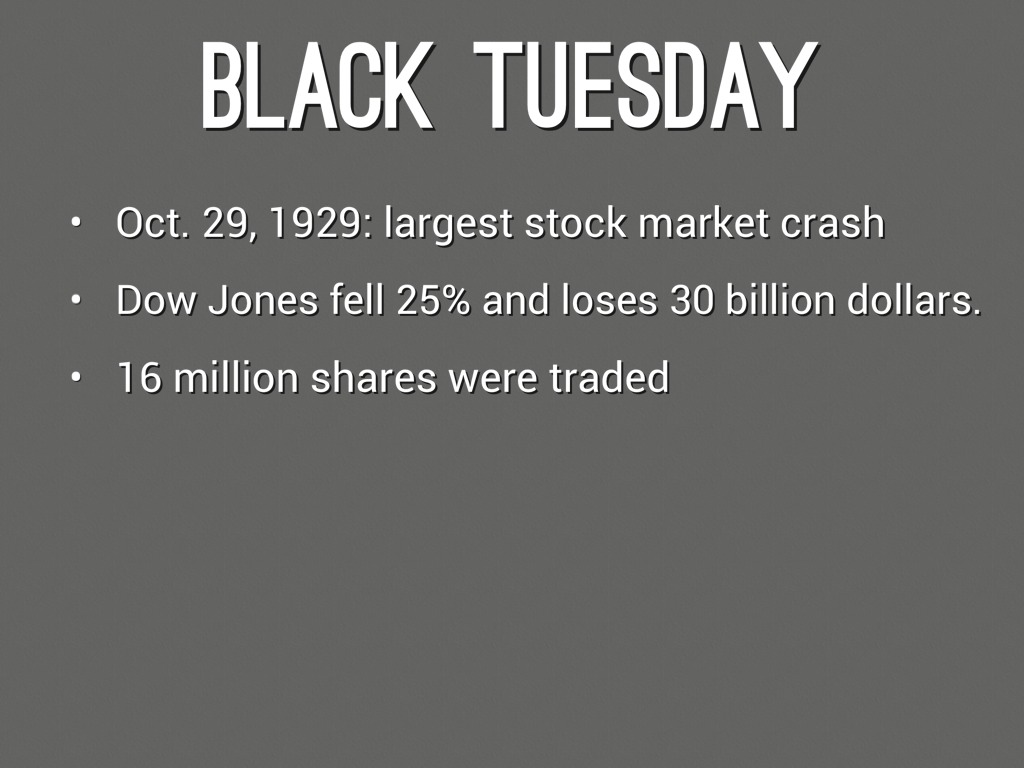

However, as the market convulsed on Black Thursday, October 24, and again on Black Tuesday, October 29, the New York Times reported, “Rally at close cheers brokers, bankers optimistic.” Yet, in a sharp editorial on October 26, the paper condemned reckless speculators and complicit analysts, declaring, “We shall hear considerably less in the future of those newly invented conceptions of finance which revised the principles of political economy with a view solely to fitting the stock market's vagaries.”

The Federal Reserve once claimed it had "insured the soundness of the business situation" as speculative markets collapsed. A century later, Alan Greenspan echoed this sentiment, testifying that bursting bubbles "need not be catastrophic" if policy mistakes are avoided. He was referring to a familiar scene: investors, fueled by borrowed money, piling into revolutionary technologies like the radio and electrification.

FrizeMedia Ghana SEO SEM Digital Marketing Proposal

The Best And Top Digital Marketing And SEO Services In Ghana

The bull market, particularly in public utility stocks, was driven by a combination of mergers, corporate restructurings, strong earnings, and company purchases for employee stock funds. Skeptics like influential banker Paul Warburg, market forecaster Roger Babson, and New York Times financial columnist Alexander Noyes were dismissed despite their warnings. Between March 1927 and March 1929, the number of brokerage accounts doubled. When the market dropped 8 percent from March 18 to 27, after a Fed-induced credit squeeze and mysterious closed-door meetings of the central bank's board, bankers stepped in to stabilize prices.

The New York Times noted that "responsible bankers agree that stocks should now be supported, having reached a level that makes them attractive." By August, the market had surged 35% from its March lows. However, it peaked on September 3 and had been in decline ever since. On October 14, just five days before "Black Thursday," Business Week offered this optimistic forecast: "Now, of course, the crucial weaknesses of such periods, price inflation, heavy inventories, over-extension of commercial credit, are totally absent."

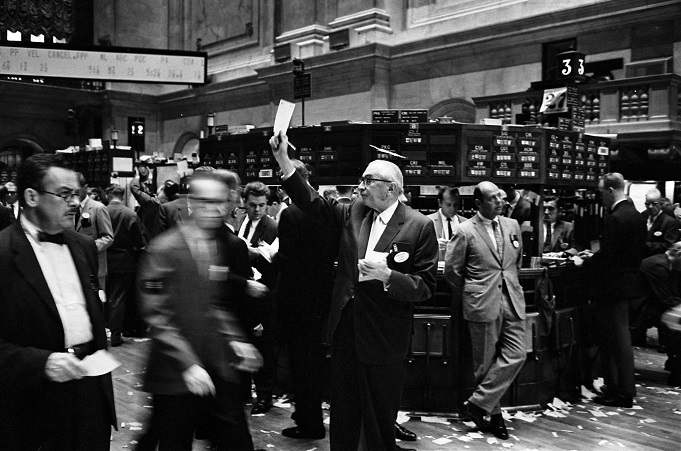

The market initially appeared to be suffering from little more than a temporary setback. Furthermore, there was confidence in the banking system, which stood ready with healthy reserves to provide liquidity if the economy showed further signs of weakness. However, the crash unfolded gradually. Despite the panic of Black Thursday, the day ended with a surprising rally. Trading resumed on Friday and continued on Saturday, the market was closed only on Sundays, bringing an initial upswing followed by modest profit-taking. The real collapse came on Monday, with the market plunging 12.8 percent. Watching from the visitors' gallery was Winston Churchill, who personally witnessed an estimated $10 to $14 billion in value evaporate.

The Wall Street Journal cautioned inexperienced investors, noting, "Many are anticipating intermittent technical corrections, yet such fluctuations are not expected to disrupt the overarching upward trajectory for long." The very next day, the market suffered a further 11.7 percent decline, though it managed to close with a significant recovery from its lowest point. October 31 proved to be a strong session, marked by a "vigorous, buoyant rally from bell to bell." Even John D. Rockefeller joined the throngs of buyers.

Shares surged, signaling that the worst may have passed. The New York Times struck an optimistic tone, suggesting that stocks would soon find their footing based on true value. Prices, the paper noted, would now be guided by each security’s fundamentals, dividend history, earnings, and future prospects, resulting in a market where some stocks rise and others fall according to their worth. Notably, the article observed, there was little mention these days of schemes to artificially inflate prices.

But it wasn't long before furious investors began attributing their devastating losses to the counsel of their stockbrokers. Alec Wilder, a New York songwriter during the 1929 crash, recalled in a conversation with Studs Terkel forty years later for Hard Times a telling moment with his financial advisor: "I sensed disaster when I heard bellboys and everyone else chattering about the market. About six weeks before the Crash, I convinced my mother back in Rochester to let me speak with our family advisor."

I intended to sell some stock my father left me. But when I mentioned it, he got sentimental. "Your father wouldn't have wanted that," he said, with such conviction that I agreed to hold onto it. At the time, it was worth $160,000. Four years later, I sold it for just $4,000.

Meanwhile, the brokerage firms, reeling from the chaos of non-stop trading and a backlog of paperwork, successfully lobbied the exchange to shut down for two days just to catch their breath.

Exchanges throughout North America quickly followed suit. Initially, the Federal Reserve resisted lowering the discount rate, insisting that financial conditions did not warrant such action, though it did intervene by purchasing government bonds to inject liquidity into the money market. Eventually, the Fed relented, partially, reducing the New York discount rate by a full percentage point. Curiously, this rate had stood 1 percent higher than those of other Federal Reserve districts. The move, however, was too little and too late.

After November 1, the market never looked back. Even with the discount rate slashed further to 4 percent, it ultimately plunged 89 percent in nominal value by the time it bottomed out three years later. No one saw it coming. Wealthy investors were stripped of their fortunes in a single day. Small-scale margin traders, the precursors of today's day traders, were wiped out, losing everything in the chaos.

From The New York Times: "Yesterday's crash largely impacted wealthy individuals, institutions, investment trusts, and other sophisticated players who participate in the market on a substantial and informed scale."

The sell-off was not driven by margin traders but by wealthy investors capable of moving large blocks of shares, ranging from 5,000 to 100,000, in high-priced stocks. They sold indiscriminately, much like the small traders who were caught in the initial market upheaval. Even the lowest prices from last Thursday now appear high in comparison to current levels. For many market participants, this downturn is particularly shocking because they have only experienced bull markets. Furthermore, selling from overseas, especially Europe, played a major role.

Some conspiracy theorists have advanced even more dramatic claims. Webster Tarpley, for instance, in his work British Financial Warfare, posits that the 1929 Wall Street crash was not a natural market correction but a deliberate act of economic warfare. Tarpley, whose assertions have found some support in contemporary publications like The Economist, specifically alleges that Montagu Norman, Governor of the Bank of England from 1920 to 1944, orchestrated the collapse. According to this theory, Norman sharply increased the British bank rate in the autumn of 1929, a move designed to repatriate British capital from New York and, in doing so, deliberately destabilize the U.S. markets and trigger their implosion.

This triggered a severe depression in the United States and beyond, marked by collapsing financial markets and sharp declines in production and employment. In 1929, Norman orchestrated a crash by bursting the economic bubble. The collapse was largely a reaction to a sudden reversal, beginning in 1928, of the Fed's "cheap money" policies, which had been designed to stimulate the economy. As Adolph Miller of the Fed's Board of Governors later explained to a Senate committee, the goal had been "to bring down money rates, the call rate among them, because of the international importance the call rate had come to acquire."

The objective was to initiate an outflow of gold, reversing the prior influx that had flowed into the United States from Britain. By that point, however, the Federal Reserve had already lost its grip on the speculative frenzy. The crash of 1929 was not without its own Enrons and WorldComs. Clarence Hatry and his collaborators confessed to falsifying the books of their investment conglomerate, fabricating a net worth of £24 million to mask the reality of £19 million in liabilities.

This triggered a forced liquidation of Wall Street positions by panicked British financiers. The downfall of Middle West Utilities, overseen by energy magnate Samuel Insull, revealed a complex network of offshore holding companies designed solely to conceal losses and mask the true extent of its leverage. Soon after, Richard Whitney, a former president of the New York Stock Exchange, was apprehended on larceny charges. In the aftermath, many analysts and commentators concluded that the stock market had become entirely detached from the conditions of the real economy.

Back then, only one in ten Americans held stocks, a far cry from the 40% who do today. Surveying the wreckage with more than a hint of Schadenfreude, The World reassured its readers that "the country has not suffered a catastrophe," suggesting the nation had merely been "gambling largely with the surplus of its astonishing prosperity." The Daily News struck a similar chord, pointing out the purely paper nature of the losses: "The sagging of the stocks has not destroyed a single factory, wiped out a single farm or city lot... decreased the productive powers of a single workman or machine in the United States."

Options Trading - Why Trade Options?

In Louisville, the Herald Post offered a shrewd observation: "While Wall Street subjected its vulnerable investors to the severest consequences, the grain market demonstrated resilience. This will contribute positively to national prosperity and help restore the consumer purchasing power that some worry has been significantly weakened."

During the Coolidge administration, as noted by the Encyclopedia Britannica, "stock dividends surged by 108 percent, corporate earnings climbed by 76 percent, and wages increased by 33 percent. In 1929, American manufacturers sold 4,455,100 passenger cars, equivalent to one vehicle for every 27 people in the country, a milestone that remained unmatched until 1950. At the heart of this economic expansion was a sharp rise in productivity."

Thanks to technological advancements, total labor expenses fell by nearly 10 percent, even as wages for individual workers continued to rise. In his influential book The Way the World Works, Jude Wanniski highlights that "between 1921 and 1929, GNP grew to $103.1 billion from $69.6 billion. And because prices were falling, real output increased even faster." During this same period, tax rates were significantly reduced. These very trends were later documented by John Kenneth Galbraith in his essential work, The Great Crash.

The late 1920s witnessed remarkable industrial growth: manufacturing establishments rose from 183,900 to 206,700 (1925–1929), with output value increasing from $60.8B to $68B. The FRB industrial production index more than doubled from its 1921 average of 67, reaching 126 by June 1929. However, this production boom was accompanied by rampant speculative behavior. Personal borrowing for consumption peaked in 1928, fueled by an "inordinate desire to get rich quickly." This consumer debt spike is particularly striking given the era's strong macroeconomic fundamentals, including twin fiscal and current account surpluses and the nation's status as a major net creditor.

Just days before the 1929 crash, Charles Kettering, who headed General Motors' research division, captured the prevailing economic logic with a phrase: "The key to economic prosperity is the organized creation of dissatisfaction." In the years leading up to that moment, inequality had grown dramatically. Although productivity, output per man-hour, rose by 32 percent between 1923 and 1929, wages increased by a meager 8 percent. By 1929, the top 0.1 percent of Americans were earning as much as the bottom 42 percent combined. Meanwhile, pro-business administrations had slashed taxes on the wealthy, reducing by 70 percent the levies paid by those earning over $1 million. Yet by the summer of 1929, a troubling sign emerged: businesses across the country began reporting sharp increases in unsold inventories.

The crash of 1929 signaled a major shift, but the market's behavior leading up to it was more complex than a simple bubble. Not all stocks were equally overvalued, and investors continued to differentiate based on perceived value. On November 3, 1929, despite the recent panic, stocks like American Can, General Electric, Westinghouse, and Anaconda Copper were still higher than they were in March 1928. Furthermore, the peak valuation, as measured by John Campbell and Robert Shiller in their Yale-published paper "Valuation Ratios and the Long-Run Market Outlook: An Update," was a price-to-10-year-earnings ratio of 28. This was high, but it was significantly lower than the 45 reached in March 2000.

In a provocative NBER working paper from December 2001, aptly titled "The Stock Market Crash of 1929 - Irving Fisher was Right", Ellen McGrattan and Edward Prescott put forward a striking argument: the 1929 crash was not a result of overvaluation. On the contrary, they contend that stocks were actually undervalued, even at the market's peak. Their detailed analysis shows that at the height of the boom, equities were trading at just 19 times after-tax corporate earnings, a multiple that pales in comparison to today's valuations, even following the recent market correction. Supporting this view, a March 1999 "Economic Letter" from the Federal Reserve Bank of San Francisco echoes the same conclusion.

It notes that at its zenith, prices reached 30.5 times the dividend yield, a figure only marginally above the historical average. This perspective stands in contrast to the argument presented by Robert Barsky and Bradford De Long in their June 1990 Journal of Economic History article, "Bull and Bear Markets in the Twentieth Century." They contend that "major bull and bear markets were driven by shifts in assessments of fundamentals: investors had little knowledge of crucial factors, in particular the long run dividend growth rate, and their changing expectations of average dividend growth plausibly lie behind the major swings of this century." Meanwhile, Jude Wanniski offers a different explanation, attributing the 1929 crash to the collapse of the Senate's pro-free-trade coalition, a political shift that subsequently paved the way for the infamous Smoot-Hawley Tariff Act of 1930.

He traces every major market shift between March 1929 and June 1930 back to the intricate protectionist danse macabre unfolding in Congress. Whether he’s right may never be settled. As for a similar crash today? It can’t be ruled out. Are we any better prepared for a repeat of 1929? Roughly as ready as we were in 1928. Human nature, the real engine behind market meltdowns, doesn’t seem to have changed much over the past eighty years. And if another crash does come, would a second Great Depression follow? That depends on what kind of crash it is.

The short-lived bursting of a temporary bubble, such as those seen in 1962 and 1987, tends to occur independently of broader economic fundamentals. However, a significant downturn following a prolonged bull market almost inevitably triggers a recession, or worse. As economist Hernan Cortes Douglas notes in The Collapse of Wall Street and the Lessons of History, published by the Friedberg Mercantile Group, this pattern played out in London during the infamous South Sea Bubble of 1720, as well as in the United States during 1835–40 and 1929–32.

Differences Between Stocks That Are Down And Out

Understanding The Stock Market

Greed And Fear Are Major Factors In The Stock Market

What Does Your Credit Rating Say About You?

InternetBusinessIdeas-Viralmarketing Home Page

Tweet

Follow @Charlesfrize

{kind=link}

{kind=link}